It is 10 years since the Brexit referendum. From an electorate of 46,501,251 people, 17,410,742 (37.4%) voted to leave, 16,141,241 (34.7%) voted to remain and 12,949,258 (27.8%) did not vote. The UK left the EU on 31 January 2020 at 11:00 pm, but remained in the single market and customs union during a transition period lasting for a further 11 months until December 31 2020.

It is 10 years since the Brexit referendum. From an electorate of 46,501,251 people, 17,410,742 (37.4%) voted to leave, 16,141,241 (34.7%) voted to remain and 12,949,258 (27.8%) did not vote. The UK left the EU on 31 January 2020 at 11:00 pm, but remained in the single market and customs union during a transition period lasting for a further 11 months until December 31 2020.

To mark the 10th anniversary of the vote a number of articles have been written assessing the effects of Brexit. Here we look at the economic effects, as do the articles linked below. This blog updates the analysis of an earlier one, The costs of Brexit: a clearer picture.

Trade

After the referendum, extensive negotiations took place on the trading arrangements between the UK and EU that would exist once Brexit was finalised.

One possibility was ‘The Norwegian model’, which would have seen the UK join the European Economic Area (EEA), giving it access to the single market, but removing regulation in some key areas, such as fisheries and home affairs. This was ruled out in favour of a bilateral trade agreement. Three main types were available:

- Swiss model, where the UK would negotiate a series of bilateral agreements with the EU, including selective or general access to the single market.

- Canadian model, where the UK would form a comprehensive trade agreement with the EU to lower customs tariffs and other barriers to trade.

- Turkish model, where the UK would form a customs union with the EU. In Turkey’s case the agreement relates principally to manufactured goods.

The agreement reached, the Trade and Cooperation Agreement (TCA) was a version of the Canadian model. The UK would leave the single market and customs union, but there would be tariff-free and quota-free trade in goods between the UK and the EU. However, to ensure that it was EU and UK business that would benefit from these ‘trade preferences’, businesses must show that their products fulfil ‘rules of origin’ requirements.

Rules of origin. Under rules of origin requirements, when a good is imported into the UK from outside the EU and then has value added to it by processing, packaging, cleaning, remixing, preserving, refashioning, etc., it can only count as a UK good if sufficient value or weight is added. The proportions vary by product, but generally goods must have approximately 50% UK content (or 80% of the weight of foodstuffs) to qualify for tariff-free access to the EU. For example, in the case of a petrol car, 55% of its value must have been created in either the EU or UK.

Rules of origin. Under rules of origin requirements, when a good is imported into the UK from outside the EU and then has value added to it by processing, packaging, cleaning, remixing, preserving, refashioning, etc., it can only count as a UK good if sufficient value or weight is added. The proportions vary by product, but generally goods must have approximately 50% UK content (or 80% of the weight of foodstuffs) to qualify for tariff-free access to the EU. For example, in the case of a petrol car, 55% of its value must have been created in either the EU or UK.

Meeting rules of origin has created a large amount of paperwork for businesses and this has created a significant barrier to trade. What is more, exporters are required to complete import/export declarations. Also, agri-food goods are subject to strict physical border controls. These barriers have increased the costs of trade and reduced its volume.

Services. Free trade in services is not provided by the TCA. Instead, services exporters face various barriers, such as certain professional qualifications no longer being recognised in EU countries and a loss of ‘passporting’ rights that previously allowed cross-border financial operations with minimal extra permissions.

Brexit impact. Despite new barriers to trade in services, they are generally less significant than the barriers for trade in goods, particularly in a digital age. Indeed, UK services exports have held up well. Although they fell in 2020, they have grown significantly since. According to House of Commons Library Statistics on UK-EU trade (see link below):

In 2025, UK exports of services to the EU were 28% above their 2019 level in real terms. Exports to non-EU countries were 26% above their 2019 level.

UK exports of goods to the EU, however, have fared less well. In 2025 they were 14% below their 2019 level in real terms. This is partly the effect of COVID and the Ukraine war, but exports to non-EU countries were only 8% lower than 2019. According to research by economists John Springford and Anton Spisak for the Centre for European Reform (see link below), Brexit has depressed UK goods exports to the EU by 16%. According to the Office for Budget Responsibility, (see link below) both exports and imports in the long run will be around 15% lower than they would have been if the UK had remained in the EU. What is more, the growth of goods trade (exports plus imports) has fallen well behind the average of the rest of the G7. And according to British Chambers of Commerce research (see link below), 54% of UK exporters think the TCA is making it harder to export and the need for change is urgent.

The new barriers reduce market access, while lower export volumes reduce competition and economies of scale. There is less competition too from imports, with many EU firms no longer exporting to the UK because of the costs. The barriers lead to a misallocation of resources, with highly productive UK firms exporting less, with less productive firms in the UK and EU focusing purely on their domestic markets. The barriers thus impose an impediment to the exploitation of comparative advantage

Investment

Both domestic and foreign direct investment (FDI) in the UK have been adversely affected by Brexit. Bloom et al., in their paper for the NBER (see link below), estimate that by 2025, investment was 12–18% lower than it would have been without Brexit.

Both domestic and foreign direct investment (FDI) in the UK have been adversely affected by Brexit. Bloom et al., in their paper for the NBER (see link below), estimate that by 2025, investment was 12–18% lower than it would have been without Brexit.

In the early years after the referendum, lower capital investment was mainly the result of uncertainty and devoting significant resources to administrative Brexit preparations. Later it was largely the result of the trade barriers themselves. Not surprisingly, firms in the UK with high exposure to EU markets experienced a sharper decline in investment than less-exposed ones.

The end of the single market and customs union reduced the attractiveness of the UK as a hub for FDI relative to competitor countries. And UK firms were encouraged to invest in the EU to create hubs for selling within the EU, thereby allowing them to avoid the trade barriers.

According to the Bloom et al. analysis, the effect of lower investment and less competition has been a fall in UK productivity of around 3% to 4% compared to remaining in the EU. The Office For Budget Responsibility argues that the post-Brexit trading relationship will reduce long-run productivity by 4% relative to remaining in the EU.

Growth in GDP

Lower investment, lower productivity and trade barriers have had a negative impact on economic growth. According to analysis by the National Institute of Economic and Social Research (NIESR) (see link below), by the end of 2023, UK real GDP was some 2–3% lower solely as a result of Brexit – in other words, after having taken into account the effects of COVID-19 and the Russia-Ukraine war. This corresponds to a per capita income loss of approximately £850. The NIESR analysis predicts that this will rise to some 5–6% of GDP, or about £2,300 per capita, by 2035.

Bank of England data, based on surveys of chief financial officers of over 2000 firms (small, medium and large), suggest that the UK economy is some 6% smaller than it would have been without Brexit. The Office for Budget Responsibility estimates that Brexit has caused a long-run reduction in GDP of 4% as a result of a similar percentage reduction in productivity.

The growth of small and medium-sized enterprises (SMEs) has been disproportionately dampened by the compliance costs of trade with the EU. Some SMEs, especially in the food and drink sector, have ceased exporting to the EU altogether.

Labour supply and migration

Halting the right of EU workers to move freely to the UK for work created acute labour shortages in specific sectors such as hospitality, health and social care, logistics, construction and agriculture. However, while immigration from the EU fell dramatically, this was more than offset by increased immigration from non-EU countries. But this was unable to fill shortfalls in some sectors.

The loss of free movement of labour means that UK workers now face restrictions on working in the EU. These include obtaining a work visa, which requires a formal job offer, sponsorship and meeting strict salary thresholds. While business trips for meetings, conferences, trade fairs, etc. are generally exempt, if the work involves remuneration, then normally a work visa will be required. The terms of work visas vary between member states. This has created a considerable barrier for touring bands and other artists. Short-term self-employed or freelance work is highly restricted, with virtually no work permit options available for visiting UK nationals.

The loss of free movement of labour means that UK workers now face restrictions on working in the EU. These include obtaining a work visa, which requires a formal job offer, sponsorship and meeting strict salary thresholds. While business trips for meetings, conferences, trade fairs, etc. are generally exempt, if the work involves remuneration, then normally a work visa will be required. The terms of work visas vary between member states. This has created a considerable barrier for touring bands and other artists. Short-term self-employed or freelance work is highly restricted, with virtually no work permit options available for visiting UK nationals.

Because employing UK nationals now imposes extra administrative and time-consuming burdens on local EU employers, many now prioritize applicants from EU nations who can start immediately.

Articles

- Ten years on, Brexit’s economic impact is becoming clearer

- How Brexit is estimated to have hit the UK economy

- Ten years on, Britain counts the cost of Brexit

- Brexit at 10: The economy

- Brexit has been an economic failure

- Ten years after the referendum, how Brexit could have been done differently

- How Brexit has made Britain poorer – in charts

- The cost of Brexit, ten years on: The impact of leaving the customs union and single market on UK trade

- Rejoining customs union would not fix damage caused by Brexit, research finds

- The Economic Impact of Brexit

- Brexit’s impact on the UK economy

- What the NBER gets wrong on the ‘Economic Impact of Brexit’

- Brexit burden must be cut

- Brexit impact will be negative ‘for the foreseeable future,’ Bank of England governor warns

- Brexit knocked 6% off the UK economy, Bank of England company data suggests

- Brexit ten years on: the economy

- Brexit 10 years later: How the UK economy and politics changed, in charts

- Ten Years of Brexit: An Assessment of the Macroeconomic, Regional, and Sectoral Impacts

- Brexit was supposed to limit immigration – it did the opposite

BBC News, Faisal Islam (24/6/26)

Reuters, David Milliken (17/6/26)

CNN, Hanna Ziady (22/6/26)

Institute for Government: Comment, Giles Wilkes (16/6/26)

LSE Blogs, Thomas Sampsos (16/6/26)

The Conversation, Renaud Foucart (22/6/26)

The Guardian, Richard Partington (14/6/26)

Centre for European Reform, John Springford and Anton Spisak (18/6/26)

The Guardian, Heather Stewart (18/6/26)

National Bureau of Economic Research , Nicholas Bloom, Philip Bunn, Paul Mizen, Pawel Smietanka, Gregory Thwaites and Sasha Abrahams (revised June 2026)

UK in a Changing Europe: blog, Gregory Thwaites, Nicholas Bloom, Paul Mizen, Pawel Smietanka and Philip Bunn (4/12/25)

Julian Jessop (24/11/25)

British Chambers of Commerce (22/6/26)

Business Matters, Jamie Young (19/10/25)

Business Matters, Jamie Young (22/6/26)

UK in a Changing Europe: blog, Jonathan Portes (2/6/26)

CNBC, Joseph Wilkins and Chloe Taylor (23/6/26)

NIESR blog (19/6/26)

LSE blogs, Alan Manning (22/6/26)

Videos

The Macro Scorecard of Brexit

The Macro Scorecard of Brexit- The Regional and Sectoral Impacts of Brexit

National Institute of Economic and Social Research on YouTube, David Aikman, Jonathan Portes, Sophie Hale and Chryssi Giannitsarou (19/5/26)

National Institute of Economic and Social Research on YouTube, Anand Menon, Sir David Lidington, Adam Yousef and Sarah Hall (2/6/26)

Reports, Research, Analysis and Data

- Brexit analysis

- Brexit: research and analysis

- Brexit analyses

- Trading relationship with the EU

- Statistics on UK-EU trade

- How are our Brexit trade forecast assumptions performing?

- Revisiting the Effect of Brexit

- Net migration to the UK

OBR

UK Parliament

Centre for Economic Performance (LSE)

House of Commons Library, Ilze Jozepa, Dominic Webb and Matthew Ward (25/4/25)

House of Commons Library, Matthew Ward and Dominic Webb (12/6/26)

Office for Budget Responsibility, Economic and fiscal outlook – March 2024, Box 2.4

National Institute of Economic and Social Research, Ahmet Ihsan Kaya, Iana Liadze, Hailey Low, Patricia Sánchez Juanino and Stephen Millard (16/11/23)

The Migration Observatory, Madeleine Sumption, Ben Brindle and Peter William Walsh (27/5/26)

Questions

- Summarise the negative effects of Brexit on the UK economy.

- Why is it difficult to quantify these effects?

- How have UK firms attempted to reduce the costs of exporting to the EU?

- Why have goods exports been worse affected by Brexit than services exports?

- What difficulties would lie in the way of the UK negotiating a Turkish or Swiss model of trading relations with the EU?

- Have there been any economic benefits from Brexit and, if so, what?

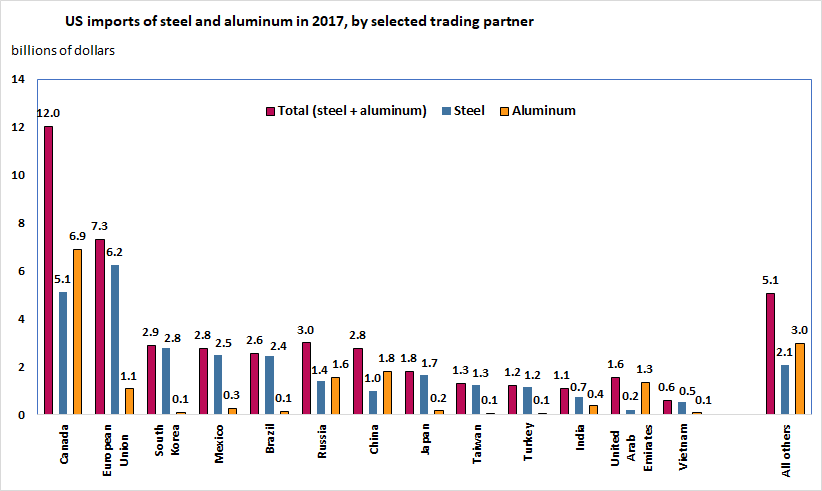

The President of the United States, Donald Trump, announced recently that he will be pushing ahead with plans to impose a 25% tariff on imports of steel and a 10% tariff on aluminium. This announcement has raised concerns among the USA’s largest trading partners – including the EU, Canada and Mexico, which, according to recent calculations, expect to lose more than $5 billion in steel exports and over $1 billion in aluminium exports.

The President of the United States, Donald Trump, announced recently that he will be pushing ahead with plans to impose a 25% tariff on imports of steel and a 10% tariff on aluminium. This announcement has raised concerns among the USA’s largest trading partners – including the EU, Canada and Mexico, which, according to recent calculations, expect to lose more than $5 billion in steel exports and over $1 billion in aluminium exports.

Why is everyone so worried about trade wars then? Trade wars, by definition, result in trade diversion which can hurt employment, wealth creation and overall economic performance in the affected countries. As affected states are almost certain to retaliate, these losses are likely to be felt by all parties that are involved in a trade war – including the one that instigated it. This results in a net welfare loss, the size of which depends on a number of factors, including the relative size of the countries that take part in the trade war, the importance of the affected industries to the local economy and others.

Why is everyone so worried about trade wars then? Trade wars, by definition, result in trade diversion which can hurt employment, wealth creation and overall economic performance in the affected countries. As affected states are almost certain to retaliate, these losses are likely to be felt by all parties that are involved in a trade war – including the one that instigated it. This results in a net welfare loss, the size of which depends on a number of factors, including the relative size of the countries that take part in the trade war, the importance of the affected industries to the local economy and others.